Small word, but extremely important in the virtual world, blockchain has arrived to revolutionize the way we do all kinds of transactions: whether through money, information or processes.

But what is blockchain?

It is a kind of distributed database that contains a chain of blocks ordered chronologically with the information stored using an extremely secure cryptographic code. Sounds complex, right? But see if you can understand it better this way: Imagine that information is the cargo of a train. Every time a car is filled with data, it gets a complex code, right? This code is made up of different types of characters, and it ends up joining the rest of the train. Thus, during this process, this code incorporates the code of the previous train into its identification. Quite simply, blockchain is a type of database that stores anything that has digital value. Thus, each new transaction is saved in a block which, in turn, is added to a chain of existing records. In other words, blockchain is nothing more than a database that computers are accessing and communicating with. In short, a blockchain is a protocol that describes how transactions are defined, connected, transmitted, and collected. Blockchain includes processes that provide consensus to update the database. Finally, was it easier to understand?

The emergence of this technology

While not yet popular, blockchain technology emerged 14 years ago alongside bitcoin in an academic paper titled “Bitcoin: A Peer-to-Peer Electronic Financial System”. The work was published under the pseudonym of Satoshi Nakamoto, the alleged creator of bitcoin at a time of global economic crisis and a housing bubble. In fact, cryptocurrency was the first to introduce this applicability in the format. However, previous attempts to create a digital financial system failed because transactions could be copied, which would allow users to spend the same money more than once. Finally, with bitcoin, the double-spending problem has been solved with the blockchain’s universal registration and confirmation processes.

And how does blockchain work?

Now that you’ve learned what is blockchain and how it came about, how about finding out how it works? But just letting you know: It’s very simple to understand! The blockchain collects information in groups, called blocks, which contain sets of data. These blocks have storage capacity and when filled, they are chained together in a sequence of other blocks also filled with the same information, forming a chain, the blockchain. In this way, all new blocks added to the chain are checked against information from their previous and newly added peers. As a result of this, an irreversible timeline of data is created. So when a new block is added to the chain, it becomes part of a conference system and timeline. And this works like this: each block has the exact timestamp of the transaction, which cannot be modified.

The Encryption

As security is a premise of blockchain, to ensure that each transaction is unique and cannot be forged, the transaction is encrypted with two keys, two codes, or passwords. Finally, with these two keys, the transaction is transformed into a block of text called a HASH. Whenever a new block is created, it carries with its content all the hash codes of previous transactions. In this way, the hash is shared with all computers connected to a network and added to the “notebook” – or database – that each unit has. This forms a kind of chain reaction of information that is tested one by one. If each block carries a hash of all previous transactions, a verification chain is generated, because all network participants can verify the veracity of all information exchanged. As a result, there is a reliable system even without a regulatory center, such as a bank or a government. Another point worth mentioning is that it is not possible to delete data or modify transactions on the blockchain. All records are permanent, form history, and can be traced, which makes it difficult to commit fraud. That is, a way to decentralize information, create an egalitarian environment for all participants, and free of scams.

The benefits of blockchain

Throughout the article, you may have noticed that blockchain technology makes the virtual world much safer. But the advantages of using it don’t stop there. See some of its benefits:

1. More transparency

Blockchain guarantees a transparent, autonomous, and fast way to make transactions and record information. However, the privacy of its users can be guaranteed, since there is the possibility of using pseudonyms and only showing the transaction addresses. Furthermore, the data cannot be erased or tampered with. In this way, blockchain can be used, for example, to eliminate embezzlement of public resources, prevent fraud in elections and facilitate audit processes.

2. Decentralization and speed

Data is stored and processed on multiple devices with internet access, not centralized in just one location. Thus, blockchain eliminates the need for people to approve transactions or set rules. As a result, transactions between banks, for example, which can take days to clear and complete, with blockchain have their time reduced to minutes and are processed 24/7.

3. Improved identity verification

By using a blockchain system, customers or users can prevent identity spoofing. This is very interesting for closing electronic contracts or transferring ownership.

4. Improved security

Blockchain avoids altering or deleting database records, greatly improving security. Information relating to a business can be accessed openly, by any user, or only with permission. In this modality, only authorized agents can have access.

5. Removal of intermediaries and automation

The nature of the blockchain excludes the need for intermediaries, and users interact directly with each other. In this way, the distributed ledger is updated in real-time, and all data entered into the blockchain is transmitted and stored automatically.

6. Automation

The blockchain was developed so that there is no duplicity or conflicting information, so transactions that do not respect this rule are not recorded within a block.

7. Immutability

Another advantage of blockchain is that its database is immutable, that is, it consists of a record that cannot be changed and reviewed even by those who operate the database.

Is this technology only for cryptocurrencies?

No! Despite being a concept born linked to Bitcoin, blockchain is not restricted to cryptocurrencies. In fact, while invasion of privacy and content manipulation scandals appear, in addition to data leakage cases, it is blockchain technology that appears first and foremost as an effective solution to make digital businesses more trustworthy.

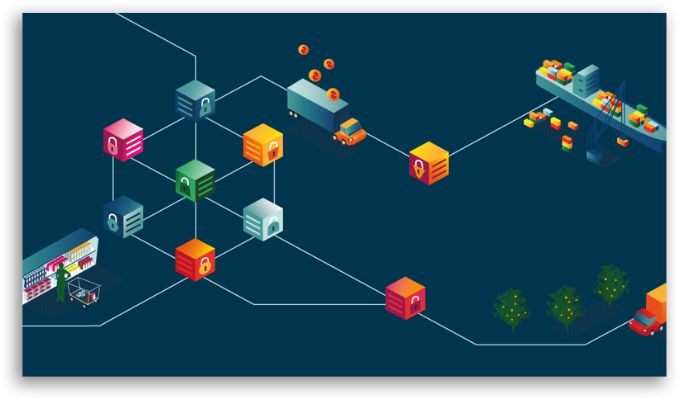

Do you want an easy example of how blockchain has already started to be used?

In agriculture, this technology tracks the food that comes to your table. And how is this done? As it is a public record, which does not depend on the company or server, all the information on that food (from its harvest until it reaches the consumer’s table) is kept on the blockchain. Thus, those who buy can know when it was harvested, how long it was stored, where it came from, etc. Cool huh? The same thing happens in the health area. By applying blockchain, it is possible to integrate and organize all data and history dispersed between hospitals, laboratories, and professionals. The result of this integration could be seen in tracking diagnoses with much more precision. In addition, if the blockchain is used in notaries, for example, it can speed up and reduce the costs of documentation processes for property registration.

Did you see how many possibilities through this technology?

This just proves how blockchain can contribute to businesses that use data entry as the basis of their operating model or that just need more reliability in their internal processes. Did you like to know what is blockchain? How about sharing it with others too?